4. SAF Accounting

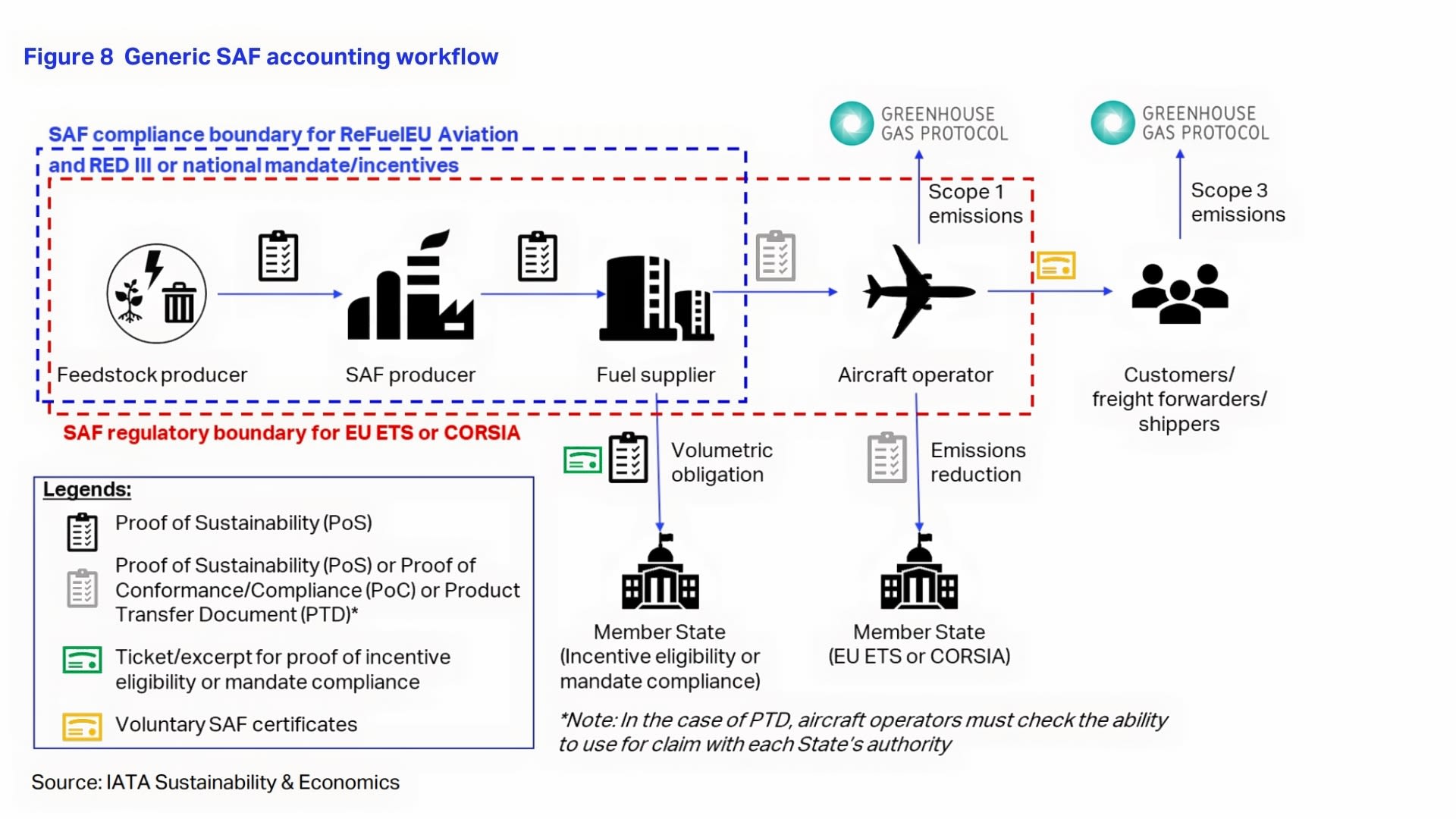

Once SAF enters the jet fuel supply chain and becomes fungible with conventional jet fuel, it is imperative to have a robust accounting mechanism in place for airlines to be able to track and claim the environmental benefit of their SAF purchases against their various decarbonization obligations.

Moreover, such an accounting system enables the separation of the environmental claims from the physical journey of the fuel – a critical element for the scaling up of SAF. Such SAF accounting should also allow aircraft operators and their customers to address their shared emissions responsibility together, while avoiding double counting and double claiming of emissions reductions thanks to transparent and credible registry systems. The general functionality of a SAF accounting system is depicted in Figure 8.

To ensure that the sustainability attributes of SAF are appropriately accounted for, traced, transmitted, and communicated, a tracking mechanism is required. This is necessary because SAF is only approved for use blended with CAF, and once they are co-mingled and used in existing distribution and fueling infrastructure along the supply chain, SAF molecules can no longer be traced independently. In the absence of an adequate accounting mechanism, the sustainability attributes can only be ascertained if the SAF remains physically segregated from the CAF, from the point of origin to the wing of the aircraft.

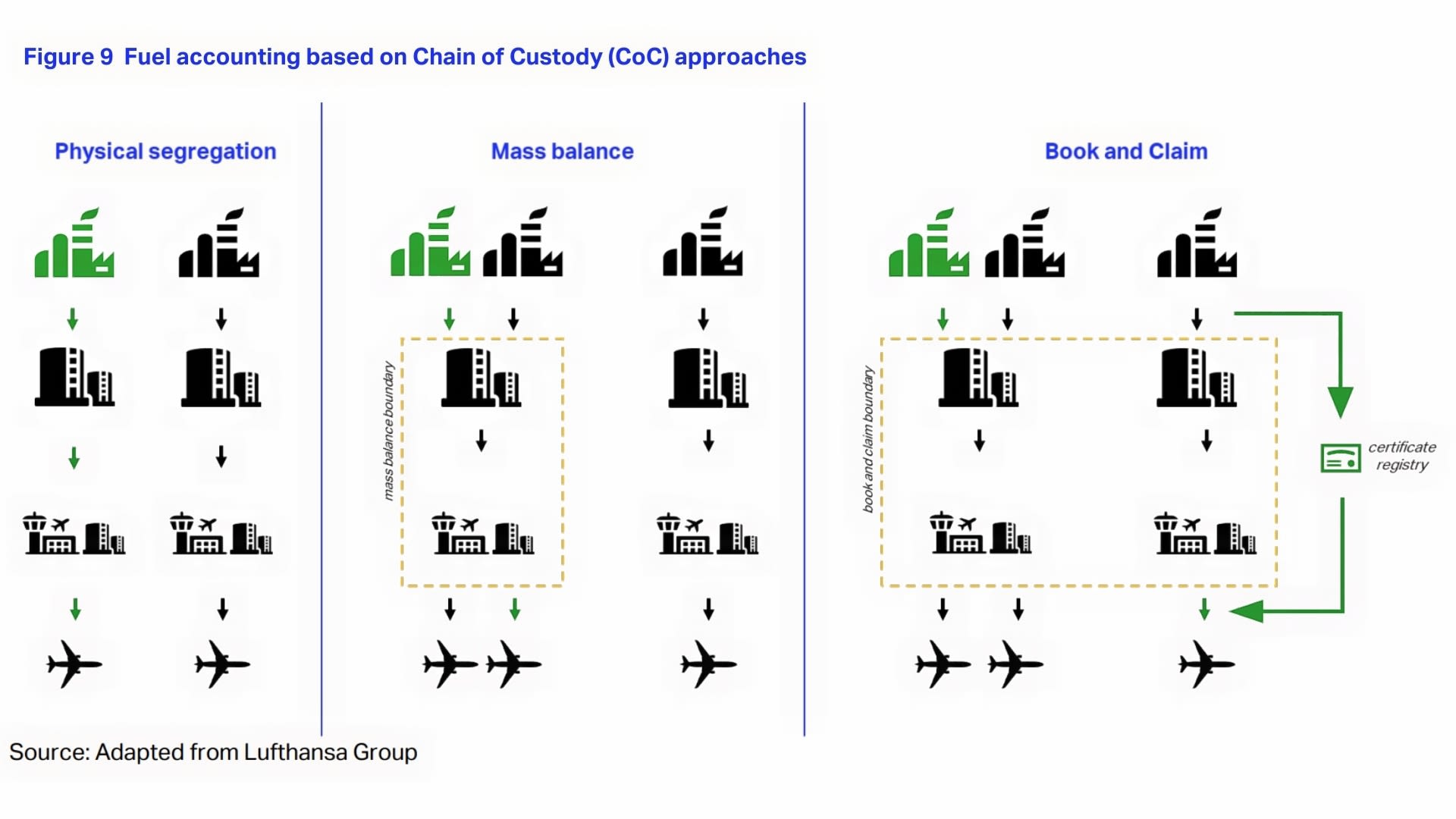

Hence, the emissions reductions associated with SAF need to be accounted for separately from the physical product, while remaining allocated to their rightful owner (i.e., airlines and their customers). This can be ensured and safeguarded with a robust SAF accounting mechanism5 based on trusted chain of custody (CoC) approaches, which have indeed been in use for jet fuel accounting for a long time and are described in Figure 9.

4.1. The Case for Book and Claim

There are different ways to account for the SAF. Two frequently referred to CoC options are mass balance, and book and claim. Mass balance allows co-mingling of SAF and CAF into common infrastructure, bur requires users to physically uplift fuel from this infrastructure.

As we are now in the very early stages of SAF market development with SAF production occurring only in a restricted number of locations, mass balance accounting will tend to preserve the current uneven distribution of SAF. This disadvantages all airlines with limited access to physical SAF. Book and claim complements mass balancing and gives access to SAF to all aircraft operators, while allowing cost efficient SAF deployment in all locations, maximizing the environmental benefits of SAF and accelerating aviation’s decarbonization.

By providing a global market for SAF, the use of book and claim can:

▪ Enable SAF production where it is most efficient

▪ Minimize logistics costs

▪ Help avoid additional emissions from transport

▪ Promote competition

In addition, transparent differentiation of SAF based on feedstocks, technologies, and GHG intensity would be possible, creating clear supply and demand signals for different types of SAF. Consequently, the use of book and claim would accelerate SAF production and deployment. CORSIA already recognizes the use of book and claim by allowing SAF use reporting based on purchase records (see section 3.1).